1) What is maritime insurance?

Maritime (or marine) insurance protects parties against financial loss tied to maritime activity: ships and hulls, cargo in transit, offshore installations, port facilities, and liabilities arising from collisions, pollution, crew injury and third-party claims. Core coverages include Hull & Machinery, Cargo, P&I (Protection & Indemnity / liability), Offshore & Energy, War & Strikes, and specialty covers such as Freight, Demurrage & Defence (FD&D).

Read more - https://market.us/report/maritime-insurance-market/

2) Market outlook (qualitative)

The market is mature and cyclical. Premium volumes and profitability move with global trade levels, shipping rates, vessel values, geopolitics and natural catastrophe frequency. Pricing typically alternates between soft periods (high capacity, competitive pricing) and hard markets (reduced capacity, tight terms, higher rates). Insurers that combine disciplined underwriting with better exposure insight are positioned to produce more consistent returns through cycles.

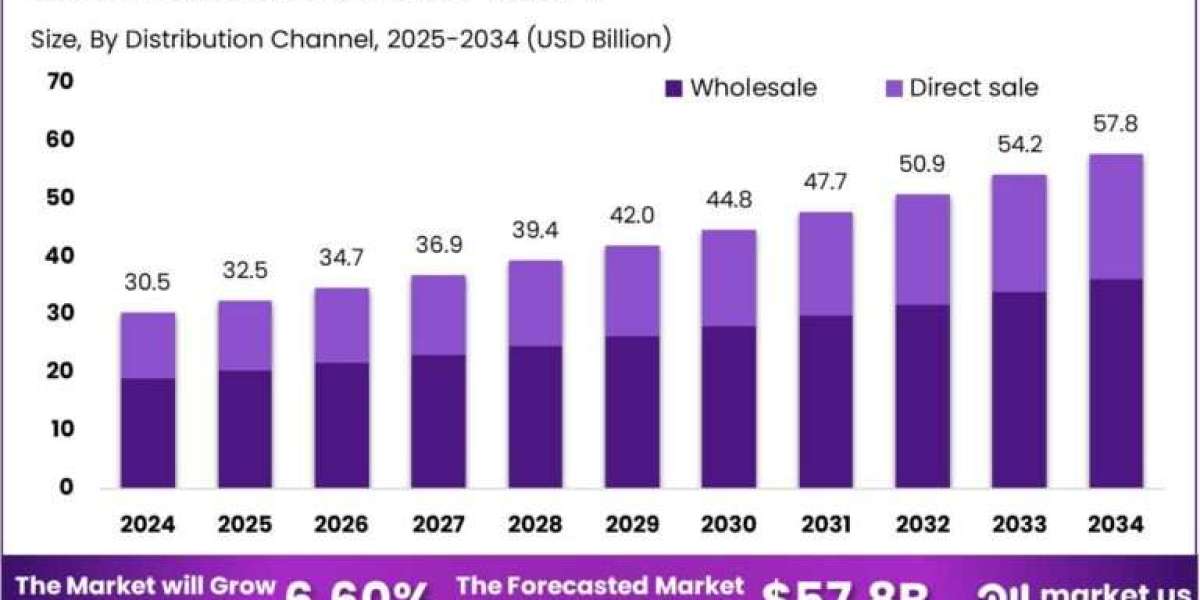

3) Market segmentation

By product: Hull & Machinery, Cargo, P&I / Liability, Offshore/Energy, War & Strikes, Specialist covers.

By customer: Shipowners/operators, charterers, cargo owners/shippers, ports & terminals, offshore operators.

By distribution: Global brokers and retail brokers, Lloyd’s and syndicates, direct insurers, mutuals/P&I clubs, reinsurers.

4) Top growth drivers

Trade value and commodity flows — as value in transit rises, insured exposure grows.

Fleet modernization and specialized vessels — higher-value newbuilds and specialized tonnage increase hull exposure.

Geopolitical tensions and regional conflicts — raise war-risk and rerouting exposures.

Climate change — increased frequency and severity of weather-related losses (storms, flooding) affecting both hulls and cargo.

Supply-chain complexity — longer routes, multimodal handoffs and just-in-time logistics increase delay and contingent exposures.