B Cell Lymphoma Treatment Market

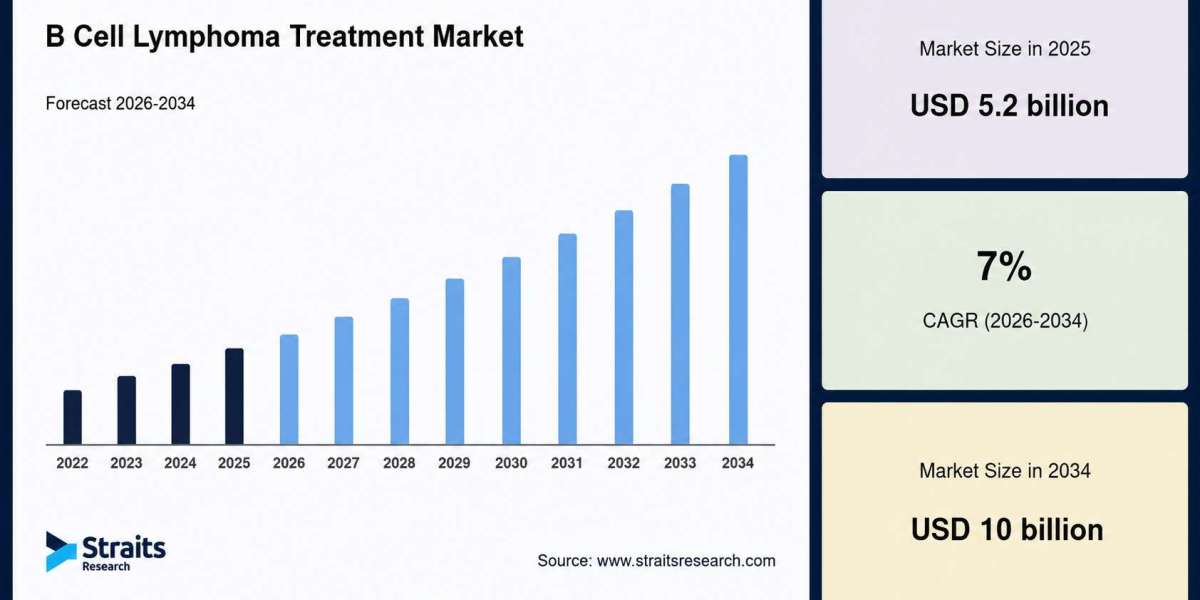

The B Cell Lymphoma Treatment Market is experiencing substantial growth as the global burden of lymphoma continues to rise and advancements in targeted therapies transform cancer treatment. The market size was valued at USD 5.2 billion in 2025 and is projected to grow from USD 5.8 billion in 2026 to USD 10 billion by 2034, registering a CAGR of 7% during the forecast period (2026–2034). Growing investments in oncology research, increasing adoption of immunotherapies, and expanding access to precision medicine are driving the market forward. Healthcare providers are increasingly incorporating innovative biologics and cell-based therapies into treatment protocols, significantly improving patient outcomes.

The growing emphasis on personalized medicine, coupled with rising healthcare expenditure and favorable regulatory support for novel oncology drugs, is further accelerating market expansion. Pharmaceutical companies continue to invest heavily in clinical trials aimed at developing next-generation therapies that offer improved efficacy with fewer adverse effects.

For detailed market insights, growth forecasts, and competitive analysis, visit: https://straitsresearch.com/report/b-cell-lymphoma-treatment-market

Market Drivers

Growing Adoption of Targeted Therapies and Immunotherapy

One of the primary growth drivers of the B Cell Lymphoma Treatment Market is the increasing use of targeted therapies and immunotherapies. Unlike traditional chemotherapy, targeted treatments specifically attack cancer cells while minimizing damage to healthy tissues, improving treatment effectiveness and reducing side effects.

Monoclonal antibodies, CAR-T cell therapies, immune checkpoint inhibitors, and antibody-drug conjugates have transformed the treatment landscape for patients diagnosed with B cell lymphoma. These advanced therapies provide better long-term disease management and are increasingly becoming part of standard treatment protocols.

Continuous regulatory approvals for innovative therapies and expanding reimbursement policies are encouraging healthcare providers to adopt these advanced treatment options across major healthcare systems worldwide.

Increasing Incidence of B Cell Lymphoma

The rising global incidence of B cell lymphoma, particularly among aging populations, continues to drive market demand. Factors such as genetic predisposition, weakened immune systems, environmental exposures, and lifestyle changes contribute to the increasing prevalence of lymphoma cases.

Growing awareness regarding early diagnosis and improved access to advanced diagnostic technologies are enabling earlier treatment initiation, thereby increasing demand for effective therapeutic options.

Expanding Research and Development Activities

Pharmaceutical and biotechnology companies are making significant investments in oncology research to develop innovative therapies for B cell lymphoma. Clinical trials evaluating novel biologics, combination therapies, bispecific antibodies, and gene-based treatments continue to expand the therapeutic pipeline, creating long-term growth opportunities for the market.

Market Challenges

High Treatment Costs

Despite significant therapeutic advancements, the high cost of B cell lymphoma treatment remains a major challenge. Advanced biologics, CAR-T cell therapies, and personalized medicines require substantial financial investment, limiting accessibility in many low- and middle-income countries.

Healthcare providers and insurance systems continue to face reimbursement challenges associated with these premium therapies, which may slow broader market adoption.

Complex Regulatory and Clinical Development Processes

Developing oncology therapies requires lengthy clinical trials, extensive safety evaluations, and strict regulatory approvals. The complexity of demonstrating long-term efficacy and safety often delays product commercialization while increasing research and development expenses.

Additionally, varying regulatory frameworks across different countries create additional challenges for global product launches.

Market Segmentation

The global B Cell Lymphoma Treatment Market is segmented by treatment type, disease subtype, end user, and region. Continuous innovation in therapeutic approaches is expanding treatment options across multiple patient populations.

By Treatment Type

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- CAR-T Cell Therapy

- Stem Cell Transplantation

- Others

Immunotherapy and targeted therapy account for a significant share of the market due to their improved clinical outcomes and lower toxicity compared with conventional chemotherapy. CAR-T cell therapy is expected to witness the fastest growth during the forecast period because of its remarkable effectiveness in treating relapsed and refractory B cell lymphoma.

By Disease Type

- Diffuse Large B Cell Lymphoma (DLBCL)

- Follicular Lymphoma

- Mantle Cell Lymphoma

- Burkitt Lymphoma

- Others

Diffuse Large B Cell Lymphoma (DLBCL) remains the dominant disease segment owing to its high prevalence worldwide and the availability of multiple targeted treatment options. Follicular lymphoma is also expected to experience considerable growth due to increasing diagnosis rates and therapeutic advancements.

By End User

- Hospitals

- Specialty Cancer Centers

- Ambulatory Surgical Centers

- Research Institutes

Hospitals continue to dominate the market because they offer comprehensive oncology care, advanced diagnostic facilities, and multidisciplinary treatment teams. Specialty cancer centers are expected to witness rapid growth as patients increasingly seek specialized oncology services and access to clinical trials.

Regional Insights

North America

North America holds the largest share of the global B Cell Lymphoma Treatment Market, supported by advanced healthcare infrastructure, strong pharmaceutical research capabilities, and early adoption of innovative cancer therapies. The United States remains the largest contributor due to significant investments in oncology research, favorable reimbursement systems, and the presence of leading biotechnology companies.

The region also benefits from extensive clinical trial activity and continuous approvals of novel targeted therapies.

Europe

Europe represents a mature oncology market with strong government support for cancer research and patient care. Countries including Germany, France, Italy, and the United Kingdom continue investing in precision medicine, advanced biologics, and immunotherapy programs to improve lymphoma treatment outcomes.

Collaborative research initiatives across European healthcare institutions further strengthen market development.

Asia-Pacific

Asia-Pacific is expected to register the fastest growth during the forecast period. Rising cancer incidence, improving healthcare infrastructure, increasing healthcare expenditure, and expanding access to advanced oncology treatments are driving regional growth.

Countries such as China, Japan, India, and South Korea are investing significantly in cancer care facilities, pharmaceutical manufacturing, and clinical research, creating attractive opportunities for global market participants.

Latin America, Middle East & Africa

The B Cell Lymphoma Treatment Market in Latin America and the Middle East & Africa is gradually expanding due to improving healthcare infrastructure, increasing cancer awareness, and greater access to specialized oncology services. Although treatment accessibility remains uneven across certain regions, government healthcare investments and collaborations with international pharmaceutical companies are expected to support future growth.

Key Players Analysis

The competitive landscape of the B Cell Lymphoma Treatment Market is characterized by strong research activity, strategic collaborations, mergers, acquisitions, and continuous product innovation. Leading pharmaceutical companies are investing in next-generation immunotherapies, targeted biologics, and cellular therapies to strengthen their oncology portfolios and improve treatment outcomes.

Key companies operating in the market include:

- F. Hoffmann-La Roche Ltd.

- Bristol Myers Squibb

- AbbVie Inc.

- Gilead Sciences, Inc.

- Novartis AG

- AstraZeneca PLC

- Eli Lilly and Company

- Pfizer Inc.

- Johnson & Johnson

- Merck & Co., Inc.

Conclusion

The global B Cell Lymphoma Treatment Market is expected to experience sustained growth through 2034, supported by continuous innovation in targeted therapies, immunotherapy, and personalized medicine. Rising disease prevalence, expanding research activities, and increasing healthcare investments are creating favorable opportunities for pharmaceutical companies and healthcare providers alike.

While challenges such as high treatment costs and complex regulatory requirements persist, ongoing technological advancements and expanding clinical research pipelines continue to improve patient outcomes and treatment accessibility. As precision oncology becomes increasingly integrated into routine cancer care, the B Cell Lymphoma Treatment Market is well positioned for long-term growth and continued innovation.

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: [email protected]

Tel: +1 646 905 0080 (U.S.)

Tel: +44 203 695 0070 (U.K.)