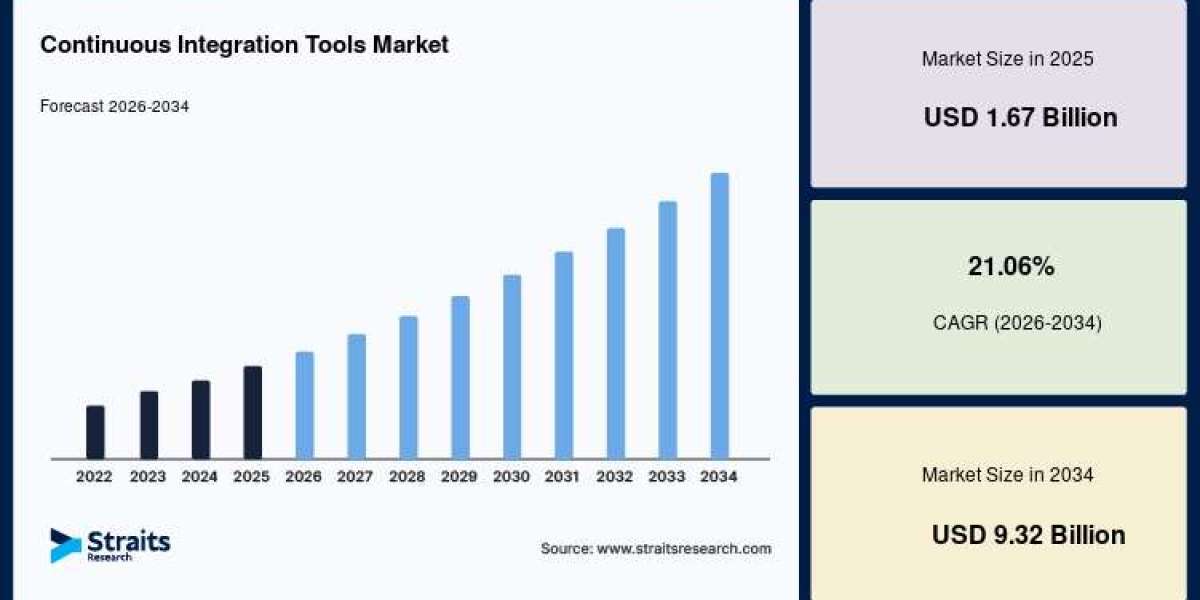

The global continuous integration tools market is witnessing remarkable growth due to increasing adoption of DevOps practices, rising demand for agile software development, expanding cloud-native application deployment, and growing investments in software automation. The global continuous integration tools market size was valued at USD 1.67 billion in 2025 and is projected to grow from USD 2.02 billion in 2026 to USD 9.32 billion by 2034, registering a CAGR of 21.06% during the forecast period (2026–2034).

Continuous Integration (CI) tools automate the process of integrating code changes from multiple developers into a shared repository, enabling continuous testing, automated builds, and rapid software delivery. These platforms improve code quality, accelerate development cycles, reduce deployment risks, and support seamless collaboration among development and operations teams. Increasing enterprise digital transformation and cloud adoption continue to fuel market expansion.

Market Drivers

Growing Adoption of DevOps Practices

Organizations are increasingly implementing DevOps methodologies to accelerate software delivery, improve collaboration, and automate development workflows, driving demand for CI tools.

Rising Demand for Agile Software Development

The growing adoption of agile development frameworks is increasing the need for automated integration, testing, and deployment solutions that support faster product releases.

Expansion of Cloud Computing

The rapid migration of enterprise workloads to cloud environments is encouraging businesses to adopt cloud-native CI platforms that support scalable software development.

Increasing Software Automation

Organizations are investing in automated testing, build management, and deployment pipelines to improve software quality while reducing manual intervention.

Growth of Microservices and Container Technologies

The increasing adoption of Kubernetes, Docker, and microservices architectures is boosting demand for CI tools capable of managing complex software delivery pipelines.

For Detailed Insights, Visit:

https://straitsresearch.com/report/continuous-integration-tools-market

Market Challenges

Complex Implementation

Deploying CI platforms within large enterprise environments often requires extensive configuration, workflow customization, and integration with existing software ecosystems.

Security and Compliance Risks

Organizations must secure CI/CD pipelines against cyber threats, unauthorized access, and software supply chain vulnerabilities.

Integration with Legacy Systems

Many enterprises face challenges integrating modern CI tools with legacy development environments and outdated software infrastructure.

Shortage of Skilled DevOps Professionals

The growing demand for experienced DevOps engineers, automation specialists, and cloud architects continues to present workforce challenges.

Market Segmentation

The continuous integration tools market is segmented based on deployment mode, organization size, application, end user, and region.

By Deployment Mode

The market is categorized into:

Cloud-Based

On-Premises

Cloud-based deployment accounts for the largest market share due to its scalability, lower infrastructure costs, rapid implementation, and support for distributed development teams.

By Organization Size

The market includes:

Large Enterprises

Small and Medium-Sized Enterprises (SMEs)

Large enterprises dominate the market owing to extensive software development operations, complex IT environments, and significant investments in DevOps automation.

By Application

The market is segmented into:

Continuous Testing

Continuous Deployment

Build Automation

Code Quality Management

Release Management

Others

Build automation represents a significant application segment due to its critical role in accelerating software development and ensuring code consistency.

By End User

The market includes:

Information Technology and Telecommunications

Banking, Financial Services, and Insurance (BFSI)

Healthcare

Retail and E-commerce

Manufacturing

Government

Media and Entertainment

Others

The IT and telecommunications sector represents the largest end-user segment due to continuous software development, cloud adoption, and rapid deployment requirements.

By Region

The market is analyzed across:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Regional Insights

North America

North America dominates the continuous integration tools market due to strong DevOps adoption, advanced cloud infrastructure, increasing software development activities, and the presence of major technology companies.

Europe

Europe holds a substantial market share supported by digital transformation initiatives, expanding enterprise cloud adoption, increasing investment in software automation, and strong regulatory compliance requirements.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth due to rapid digitalization, expanding IT services, growing startup ecosystems, increasing cloud adoption, and rising investments in software development across China, India, Japan, South Korea, Singapore, and Australia.

Latin America

Latin America is experiencing steady market growth driven by increasing enterprise digital transformation, expanding cloud infrastructure, and growing demand for agile software development.

Middle East & Africa

The region is witnessing gradual growth owing to smart government initiatives, digital economy development, increasing enterprise cloud adoption, and growing investments in IT modernization.

Technology Trends and Market Opportunities

The continuous integration tools market is evolving through innovations in artificial intelligence-powered code analysis, machine learning-based test automation, cloud-native CI/CD platforms, GitOps workflows, Infrastructure as Code (IaC), container orchestration, Kubernetes integration, and low-code DevOps solutions. Organizations are increasingly adopting AI-driven automation to improve software quality, accelerate release cycles, and optimize development pipelines.

Growing investments in cloud computing, digital transformation, DevSecOps, software supply chain security, platform engineering, edge computing, and enterprise automation are creating significant opportunities for market participants. Furthermore, increasing adoption of hybrid cloud environments and continuous delivery practices is expected to support long-term market growth.

Key Players Analysis

The continuous integration tools market is highly competitive, with leading software vendors focusing on cloud-native DevOps platforms, AI-powered automation, strategic acquisitions, and integrated software development solutions.

Major companies operating in the market include:

GitLab Inc.

Atlassian Corporation Plc

Microsoft Corporation

CloudBees, Inc.

Circle Internet Services, Inc. (CircleCI)

JetBrains s.r.o.

Red Hat, Inc.

IBM Corporation

Amazon Web Services, Inc.

Google LLC

These companies continue to invest in AI-powered CI/CD automation, cloud-based DevOps platforms, integrated software development environments, and enterprise security capabilities to strengthen their positions in the global continuous integration tools market.

Related Report

DevOps Market

https://straitsresearch.com/report/devops-market

About Us

Straits Research is a leading market research and intelligence organization specializing in analytics, advisory services, and comprehensive market research reports across multiple industries.

Contact Us

Email: [email protected]

U.S. Tel: +1 646 905 0080

U.K. Tel: +44 203 695 0070